Good evening,The latest weekly portfolio updates are now available.From time to time, we get a week where we feel that by the time we've analysed the data it's already out of date. That doesn't mean that it's not relevant; it just needs to be ...

Good evening,The latest weekly portfolio updates are now available.From time to time, we get a week where we feel that by the time we've analysed the data it's already out of date. That doesn't mean that it's not relevant; it just needs to be ...

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Last week most of the stock market indices that we track went down, thou...

Good evening,The latest weekly portfolio updates are now available.Having seen both portfolios go up pretty consistently for the last year, it's always disappointing when they take a turn for the worse. However, the losses last week were relat...

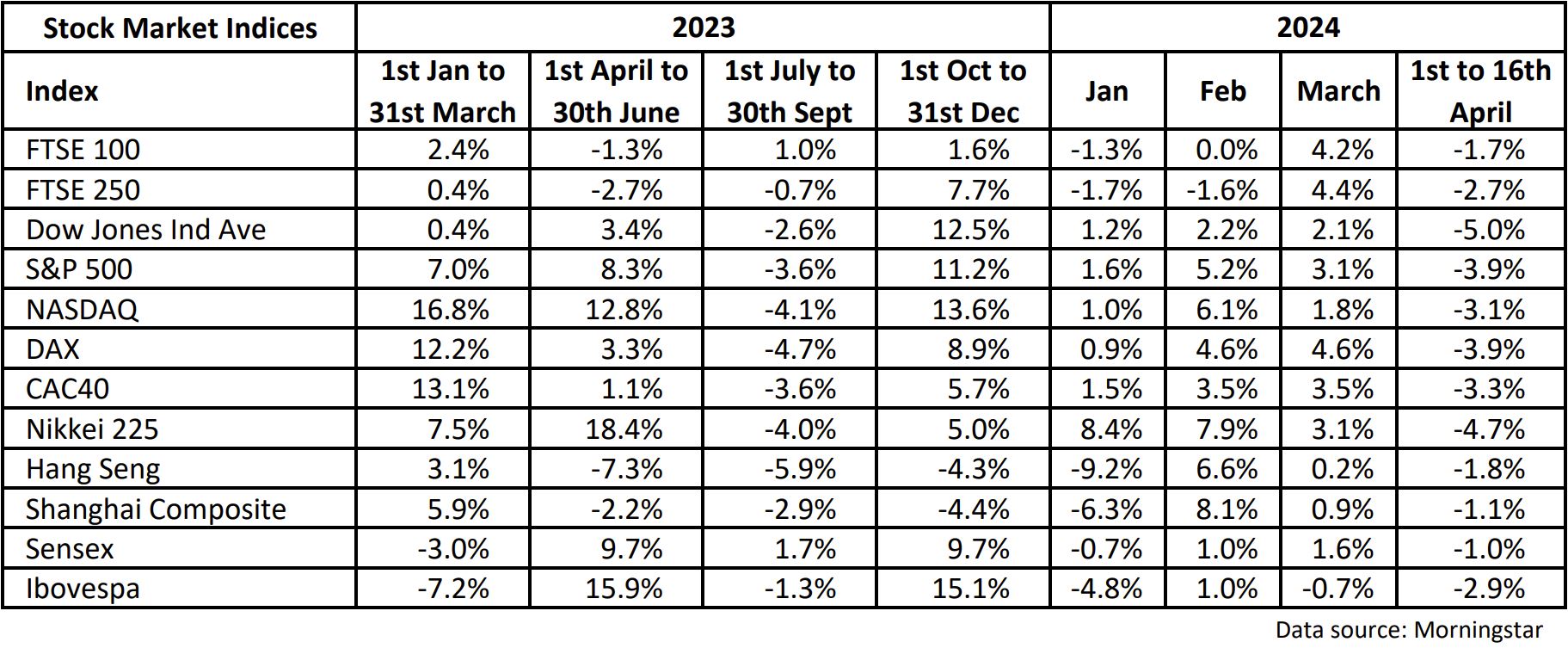

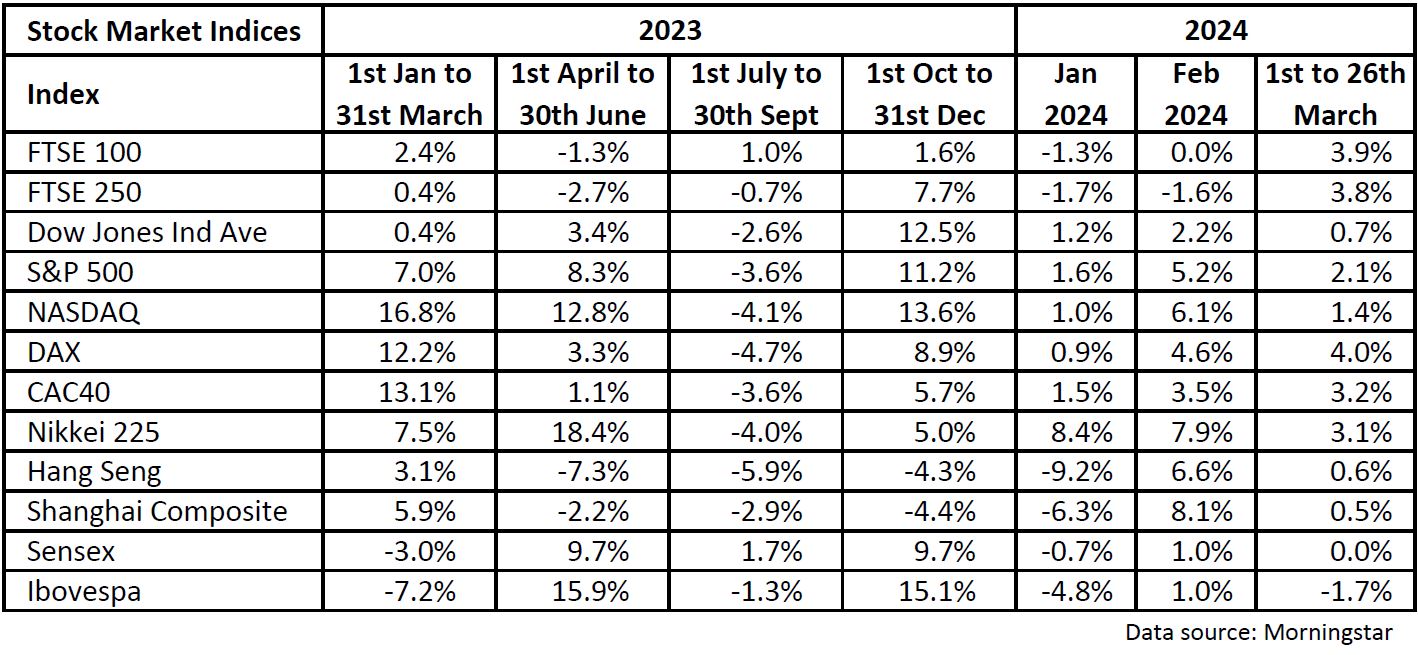

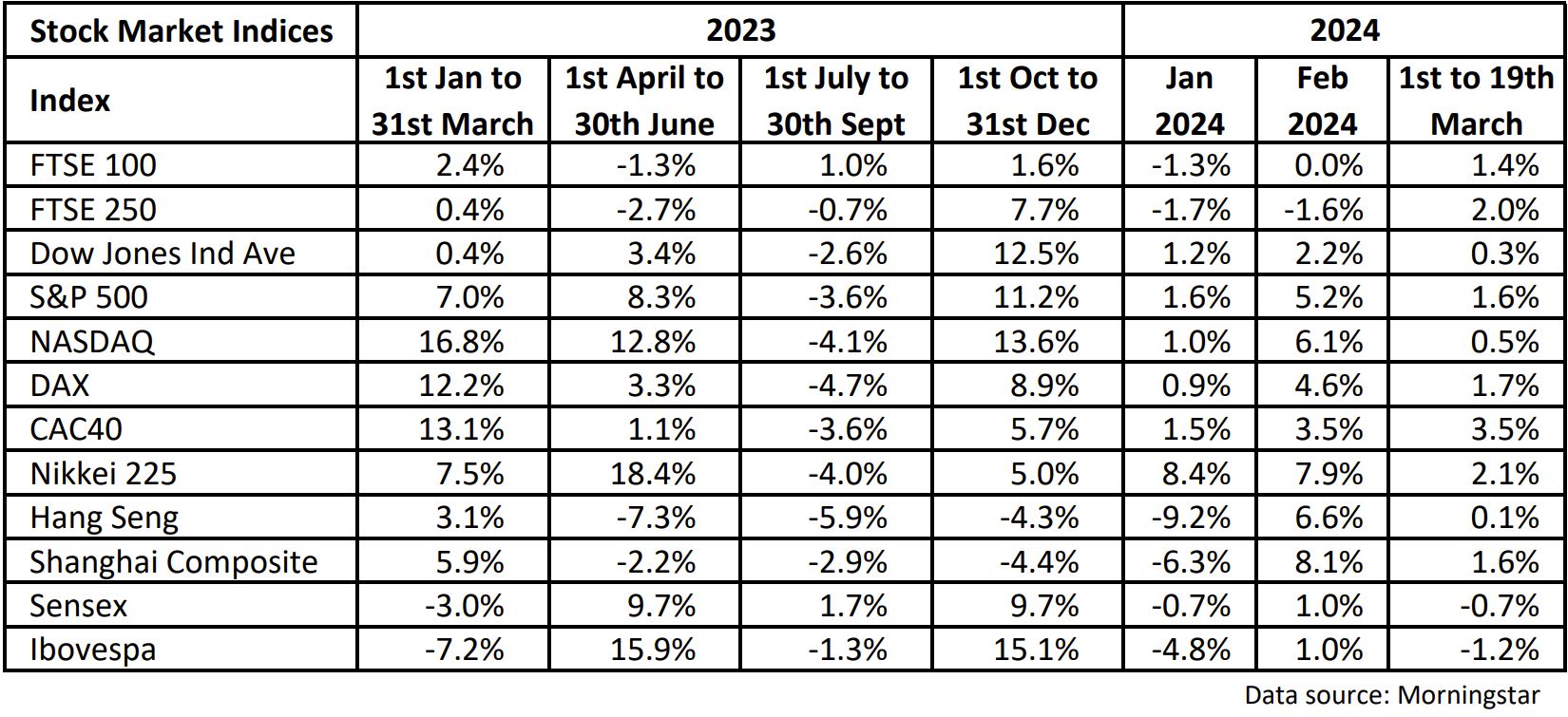

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. After an encouraging March, where nearly all of the stock markets that w...

Good evening,The latest weekly portfolio updates are now available.Because of the bank holiday weekend, stock markets have only been open for a couple of days since we last reviewed the portfolios. Nevertheless, when I looked this morning both...

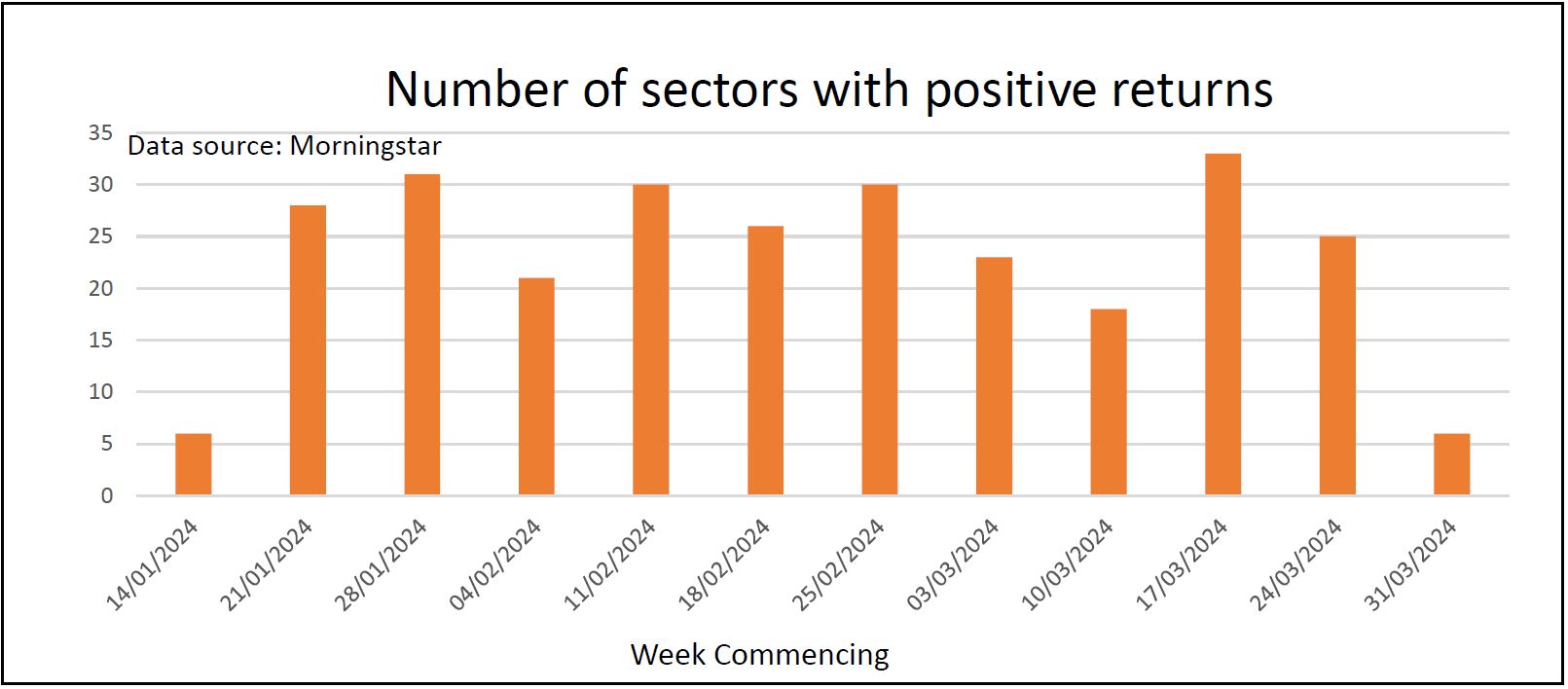

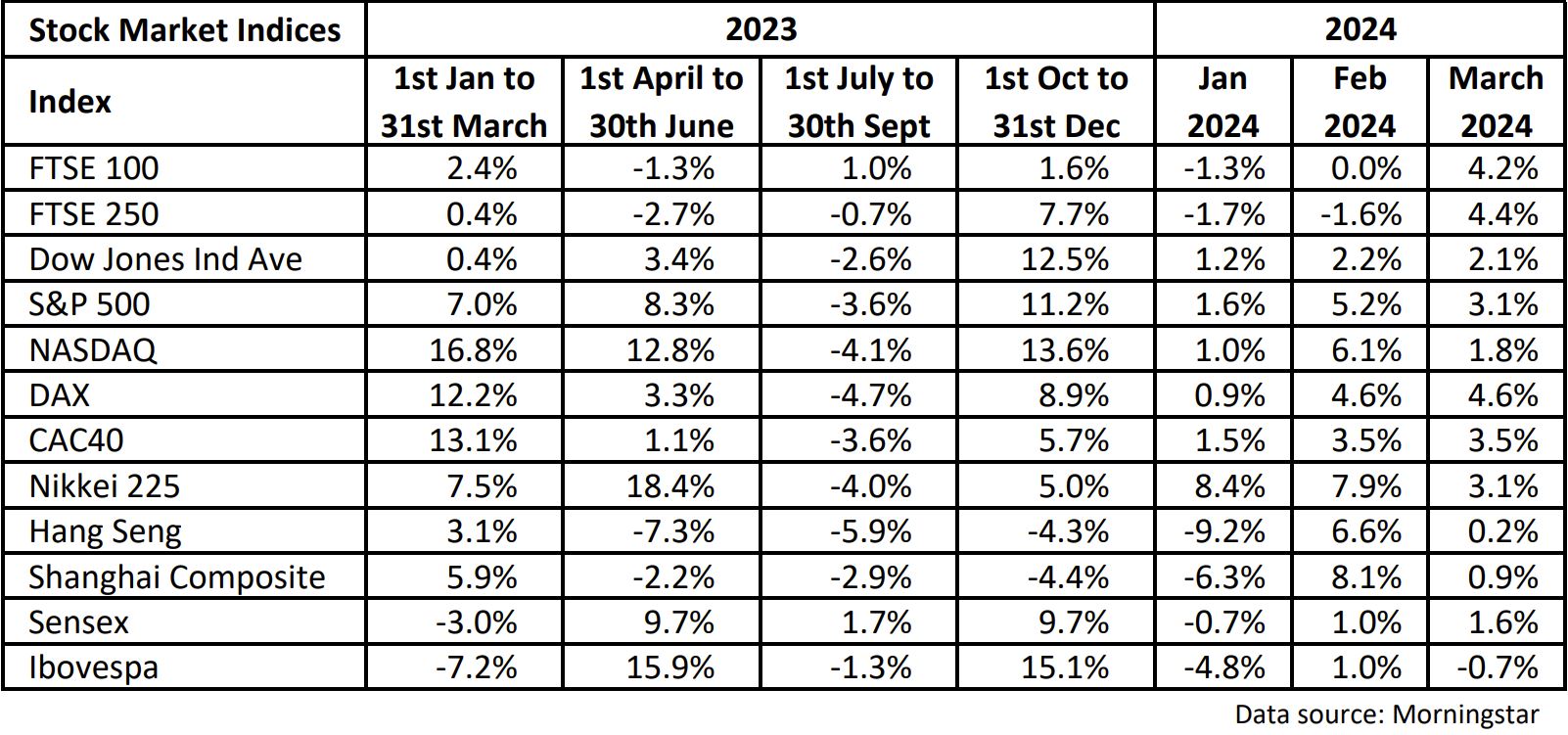

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Last week most of the stock market indices that we keep an eye on went u...

Good evening,The latest weekly portfolio updates are now available.It's always encourgaing when the portfolios are going up. Since this time last week the Tugboat has made 0.6% and the Ocean Liner is up 1.2%. I'm not saying that they're settin...

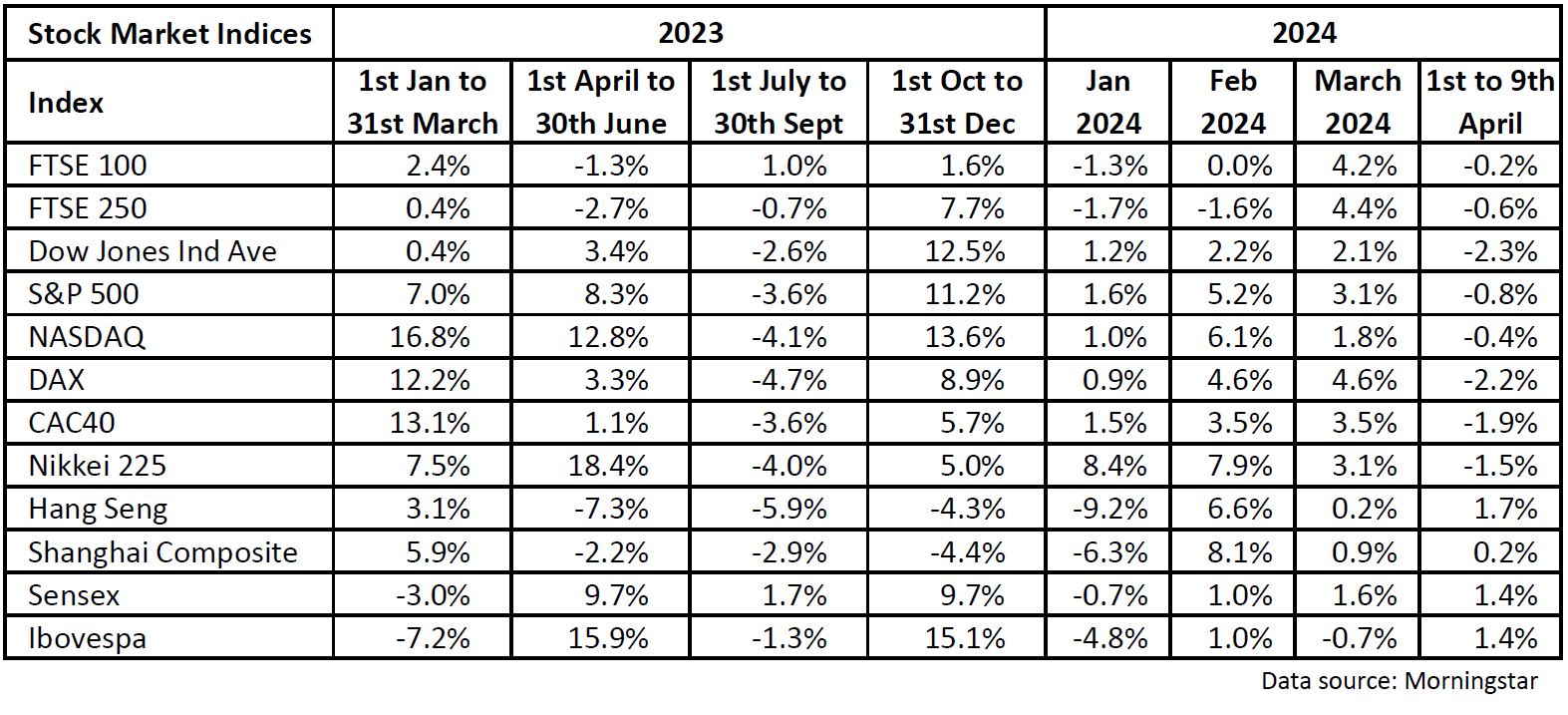

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. I'm sorry that our regular weekly update is a little bit later than usua...

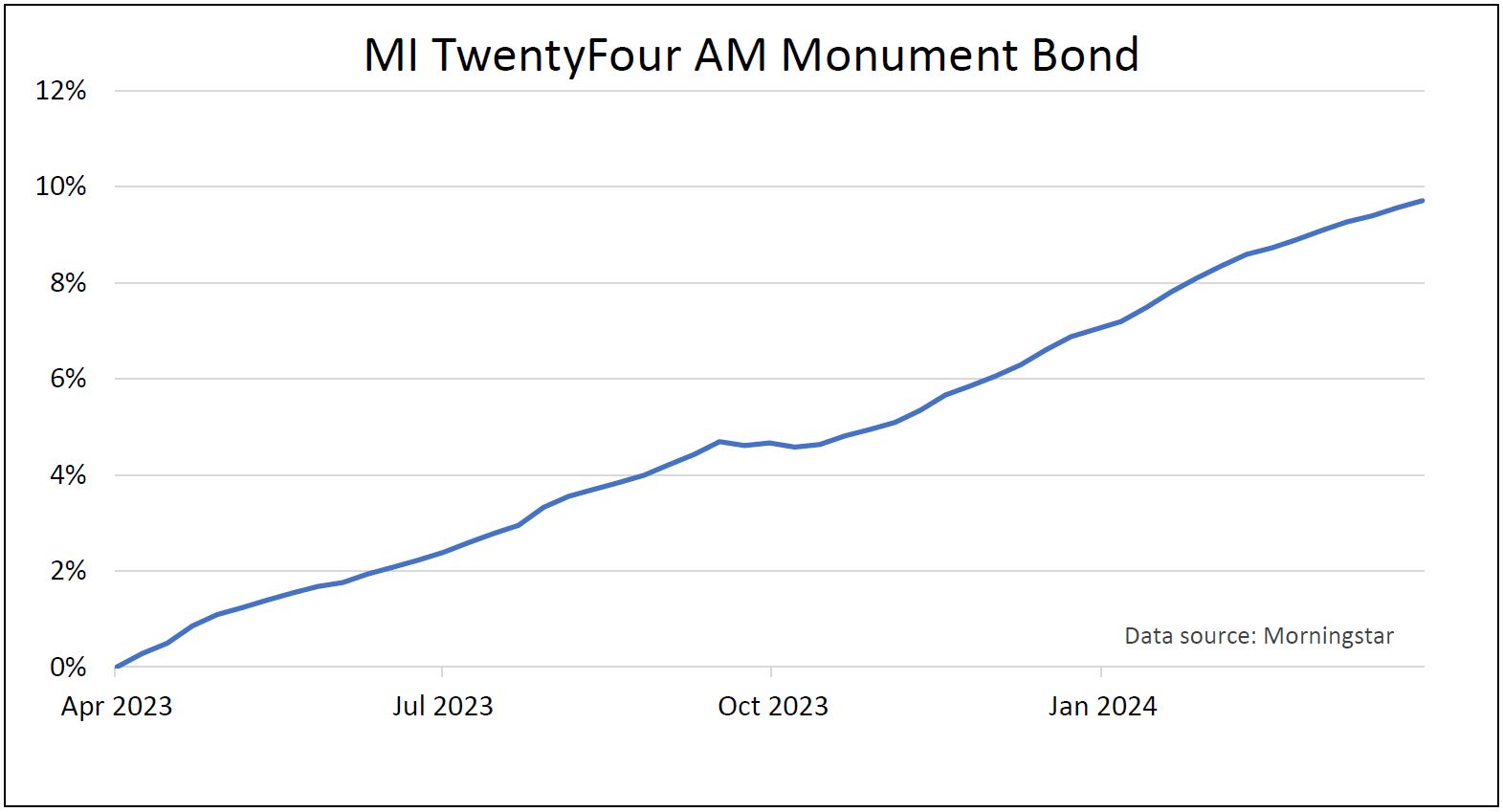

Good evening,The latest weekly portfolio updates are now available.Although nearly all of our holdings have gone up since this time last week, when I looked this morning both portfolios were slightly down. In the Tugboat it was literally by a ...

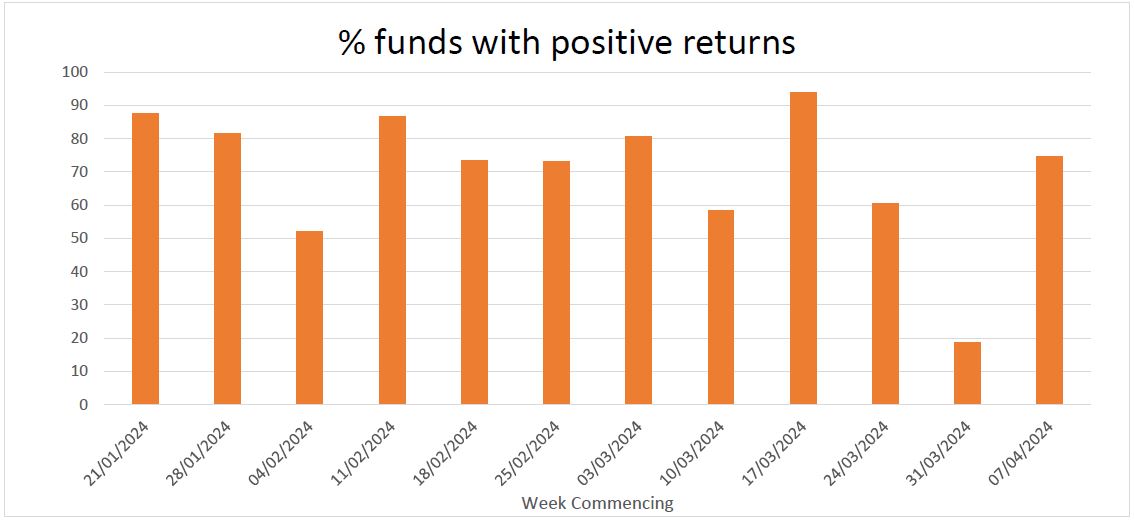

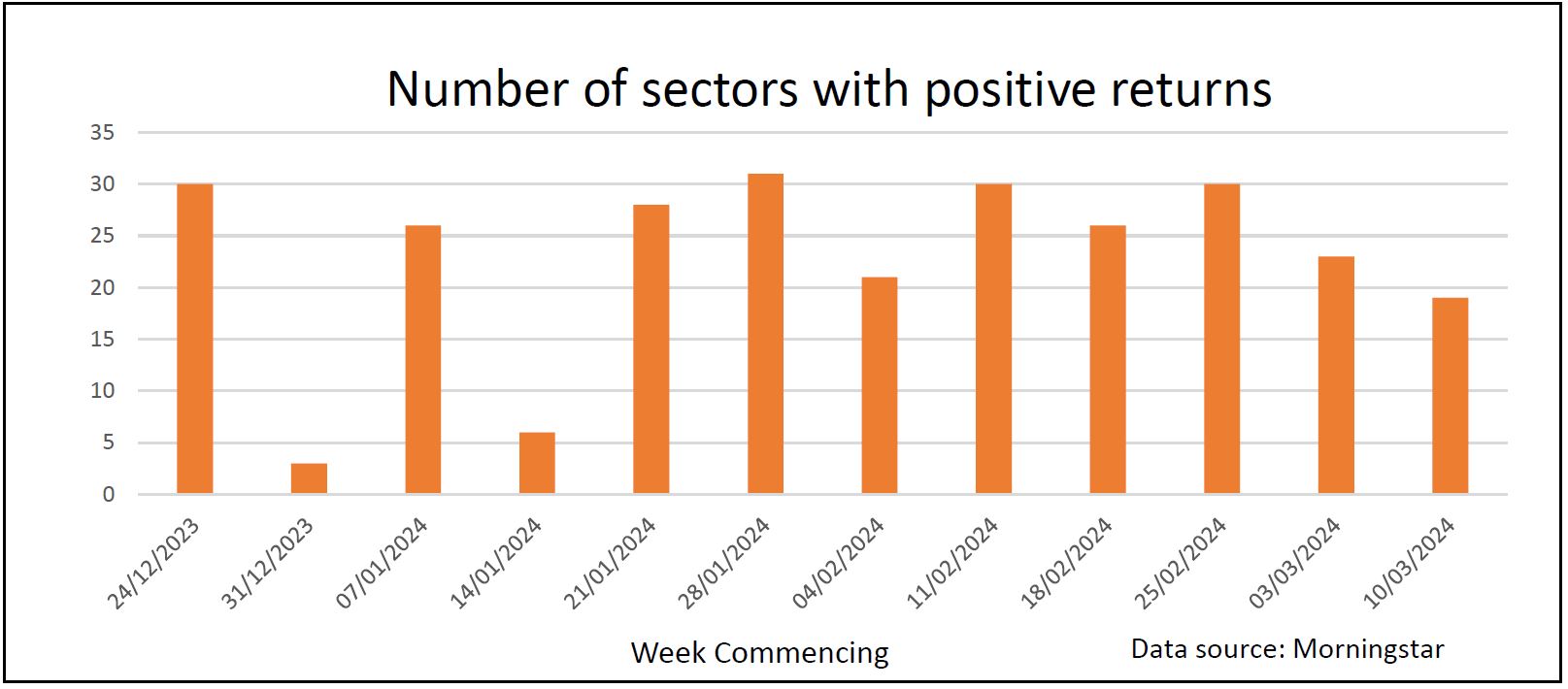

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Last week only five out of the twelve stock market indices that we regul...