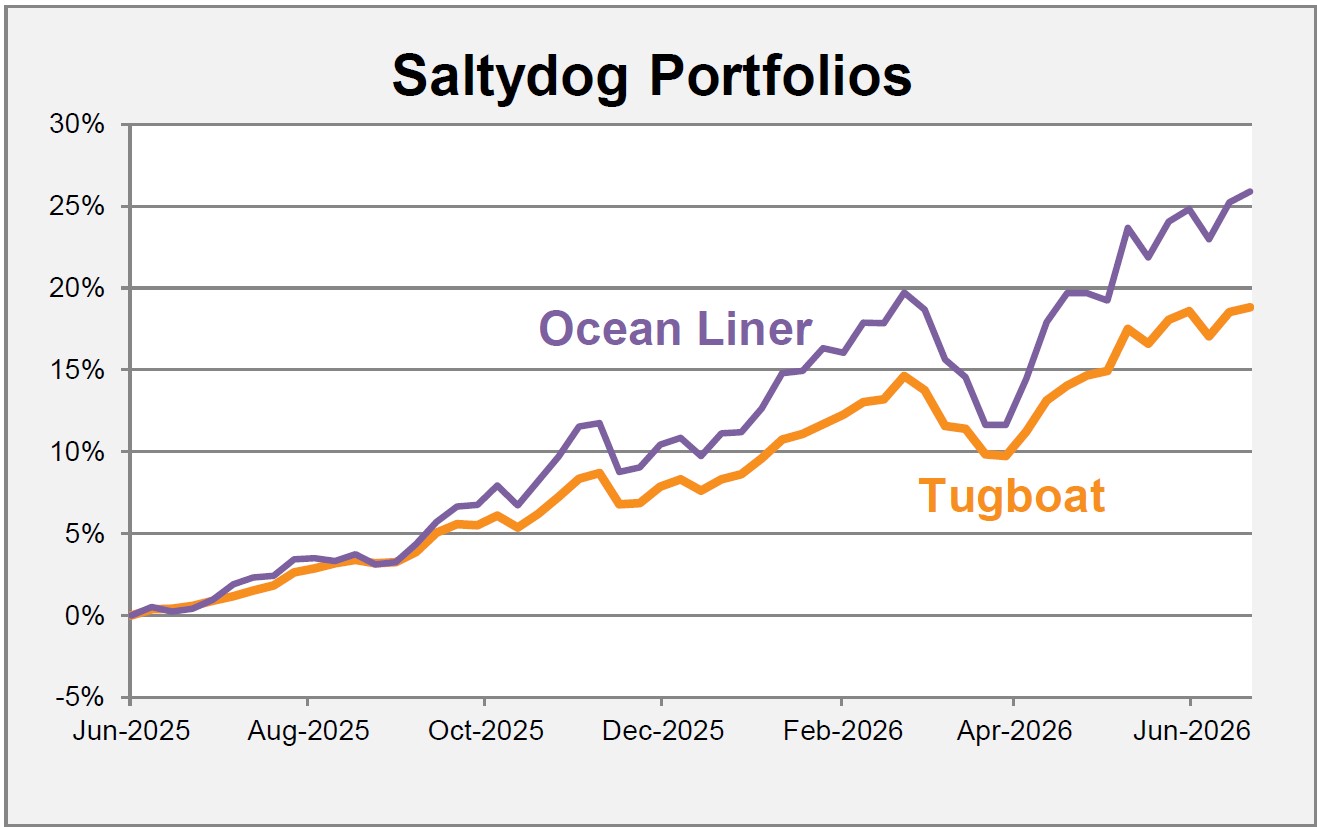

Good evening,The latest weekly portfolio updates are now available.It’s been another challenging week, and both portfolios are down over the last seven days. The Tugboat has fallen by 0.6%, while the Ocean Liner is down 0.7%.This week we are o...

Good evening,The latest weekly portfolio updates are now available.It’s been another challenging week, and both portfolios are down over the last seven days. The Tugboat has fallen by 0.6%, while the Ocean Liner is down 0.7%.This week we are o...

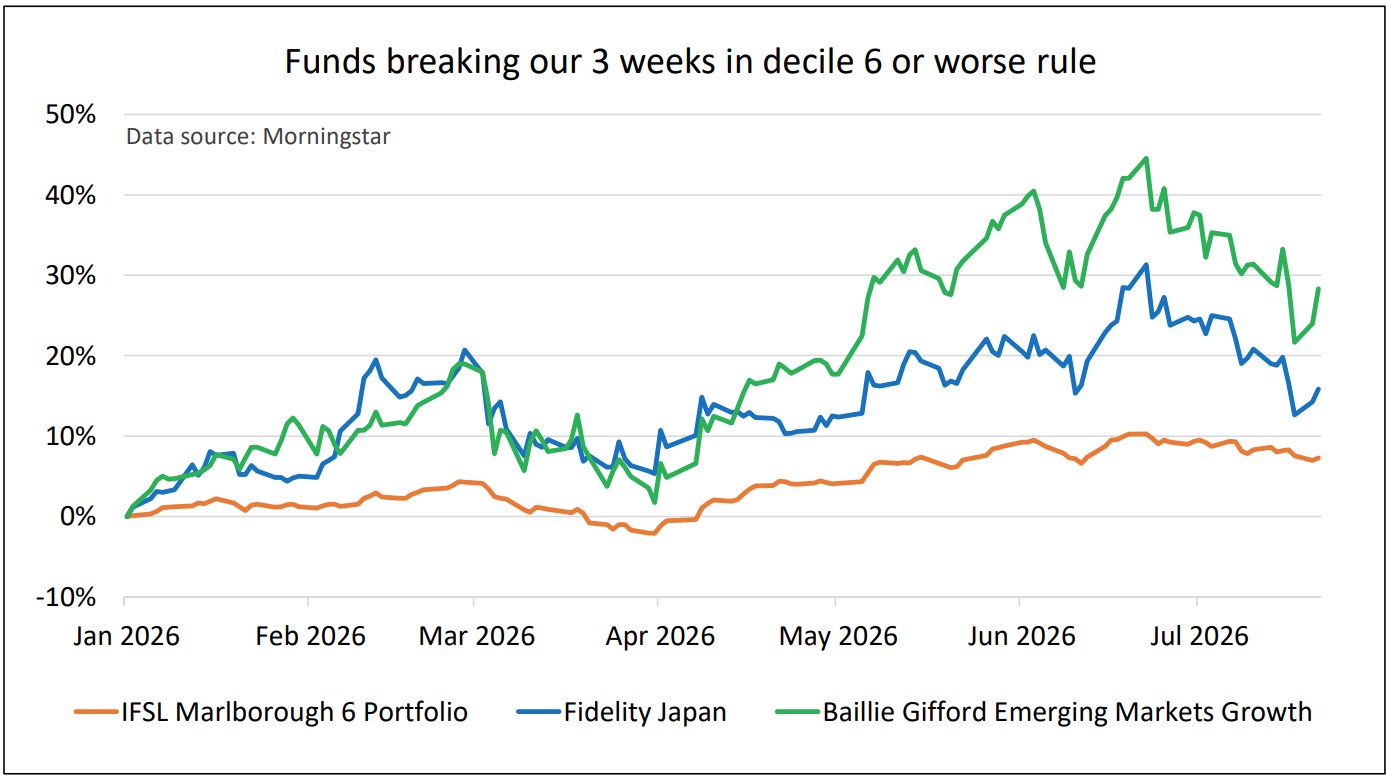

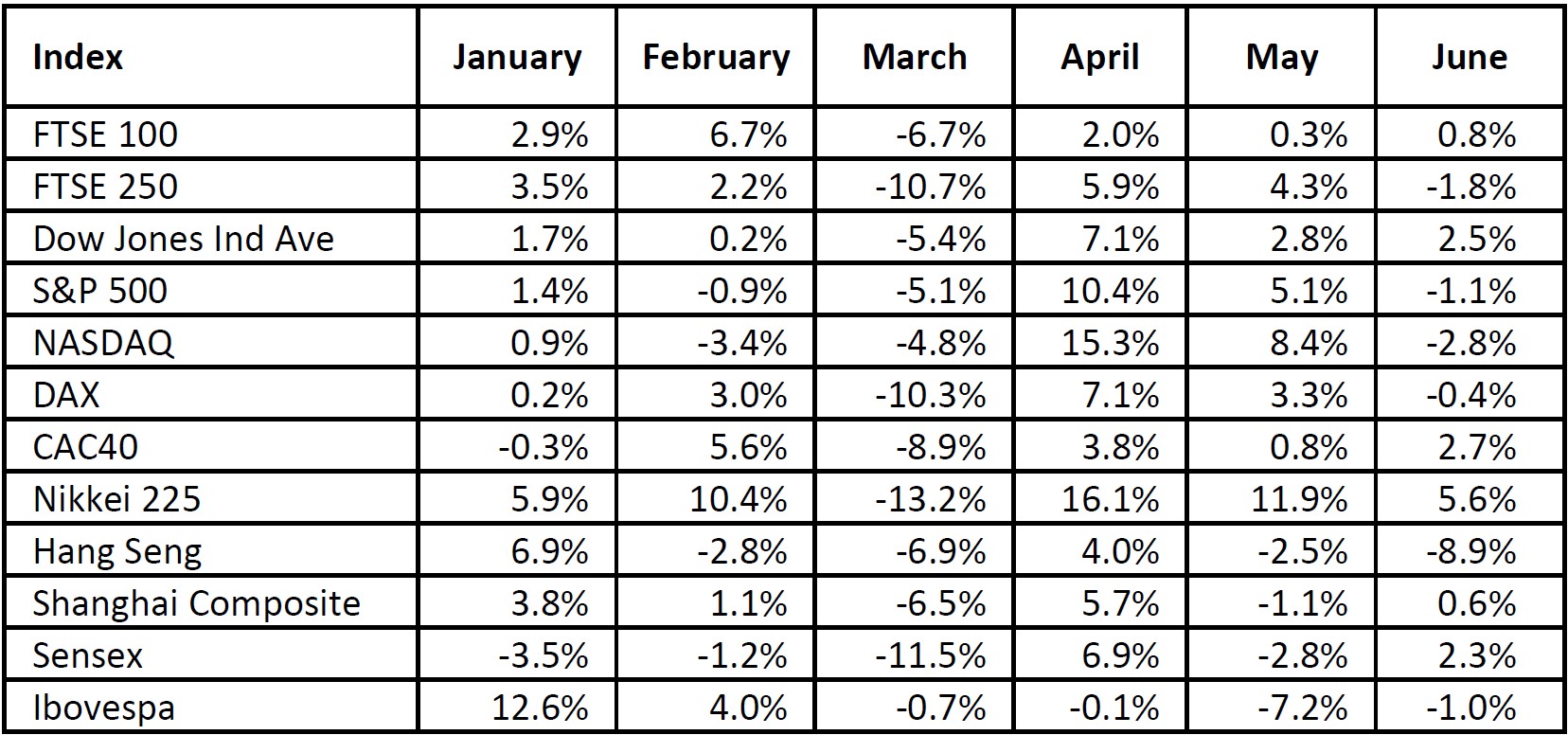

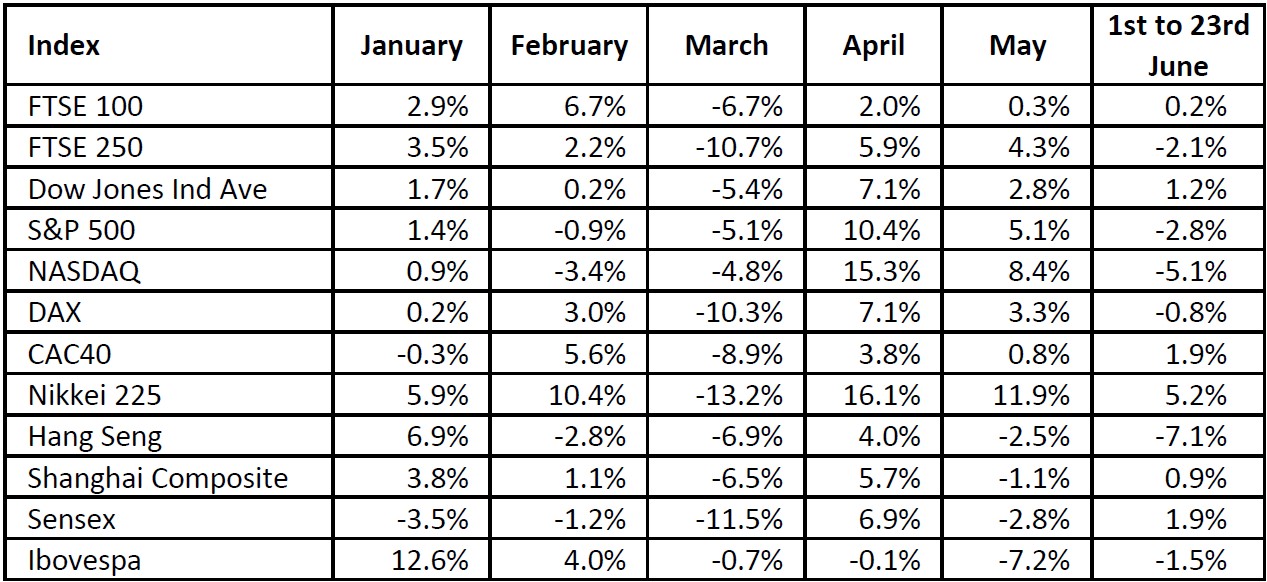

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Last week, only four of the twelve major stock markets that we monitor m...

Good evening,The latest weekly portfolio updates are now available.It’s been another difficult week for the portfolios. Having enjoyed steady gains during April, May and June, the first couple of weeks of July have been much more challenging.A...

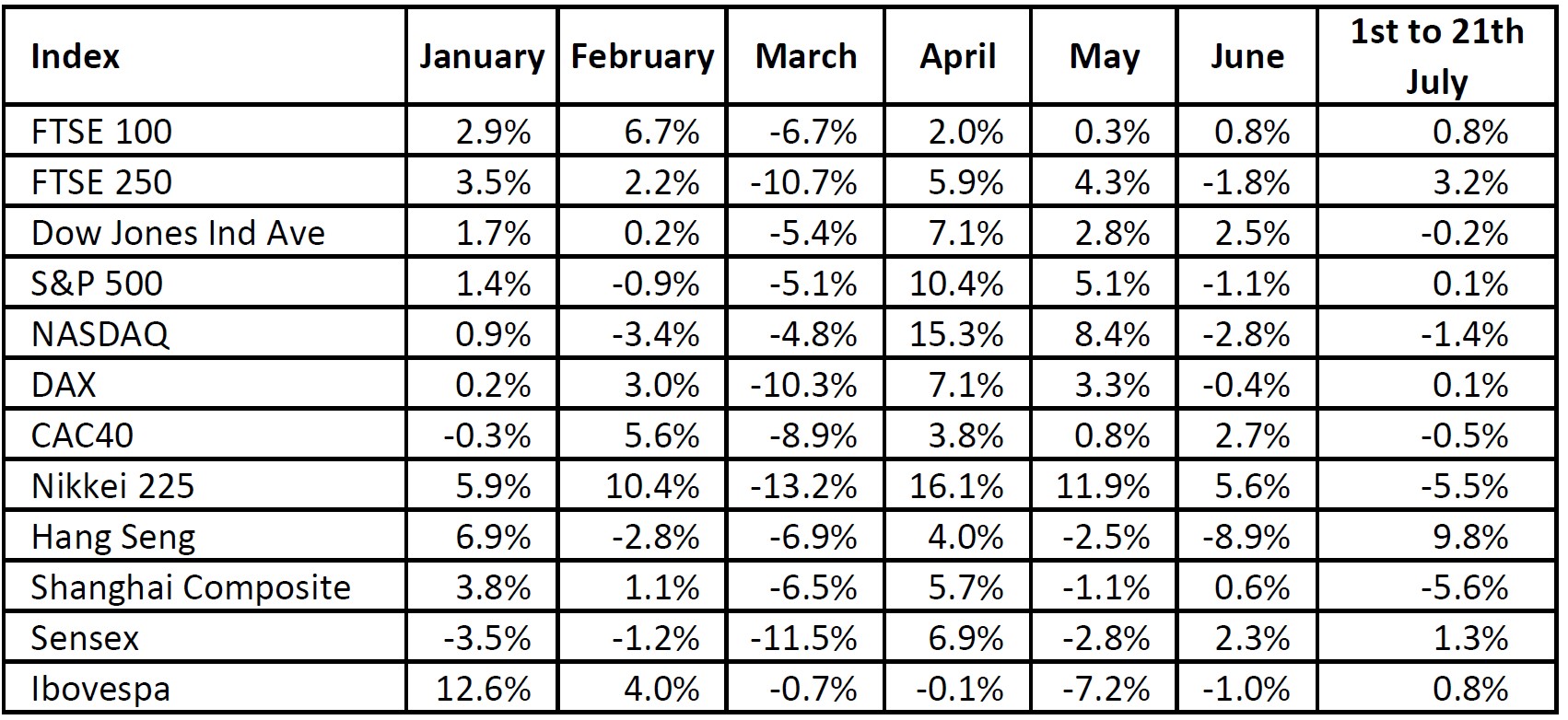

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Most of the major stock market indices that we track fell last week, wit...

Good evening,The latest weekly portfolio updates are now available.Both portfolios have gone down by 1.0% since this time last week. Most of our individual holdings have also suffered losses. The exceptions were the Janus Henderson Global Resp...

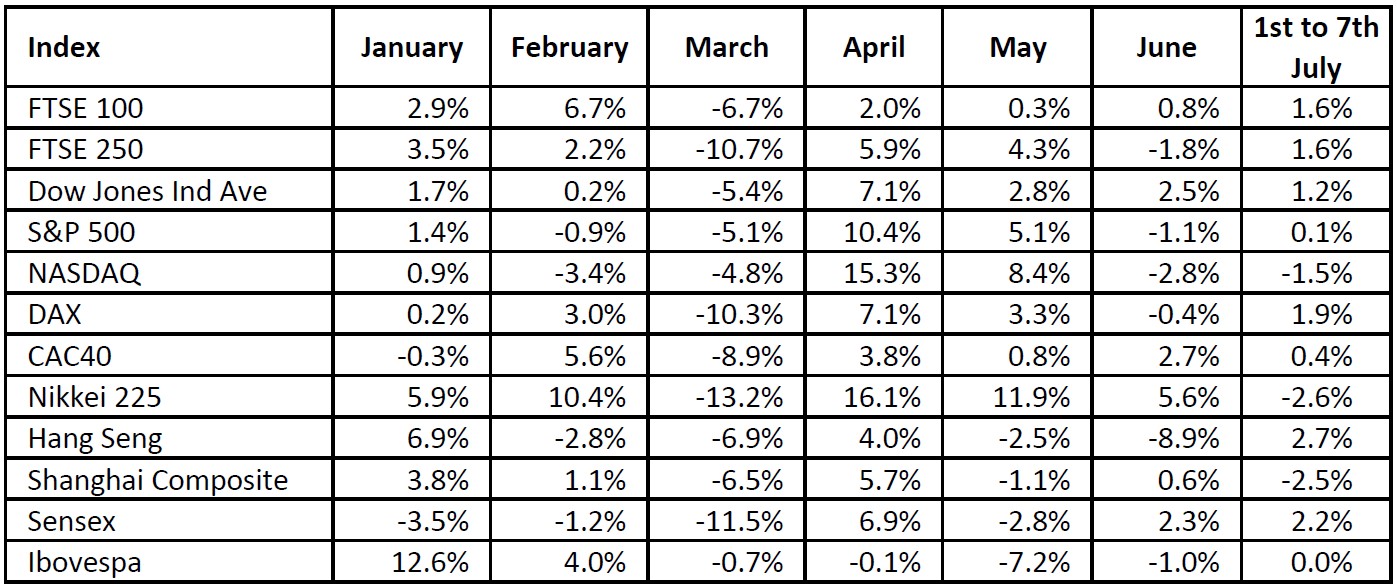

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. All of the major stock market indices that we track went up last week. G...

Good evening,The latest weekly portfolio updates are now available.This time last week, we were celebrating the fact that both portfolios had just risen to new all-time highs. Unfortunately, since then they have both drifted lower. The Tugboat...

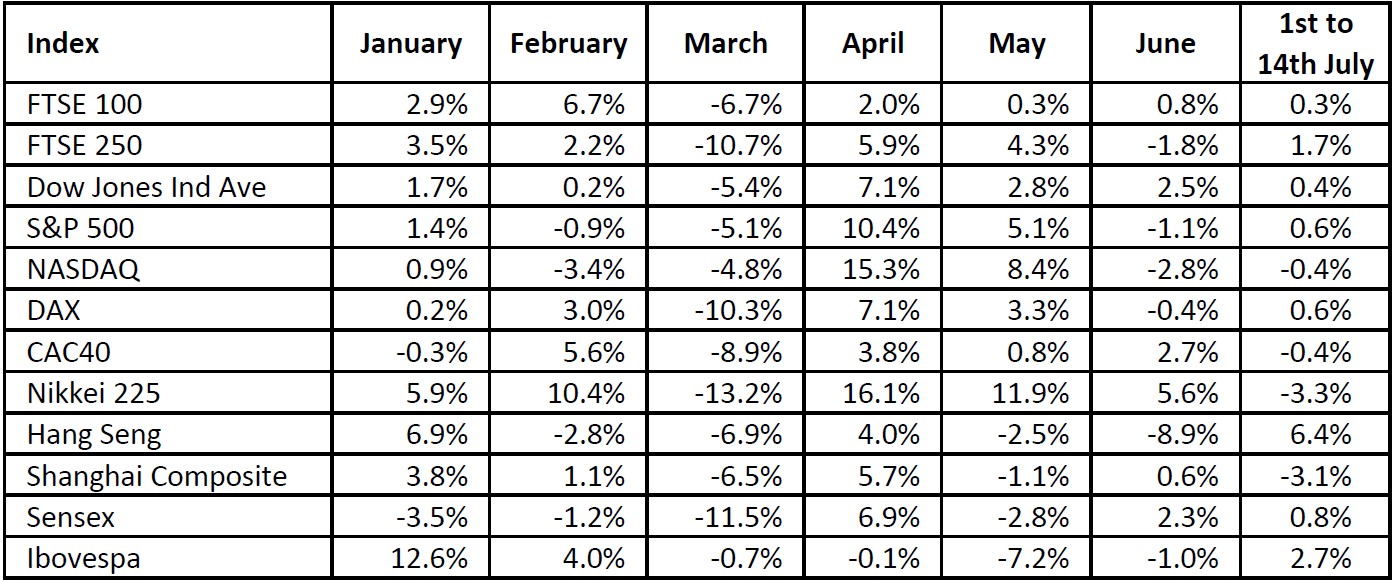

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Most of the major stock market indices that we track fell last week, wit...

Good evening,The latest weekly portfolio updates are now available.When we checked this morning, both portfolios were ahead of where they were a week ago.The Tugboat had risen by 0.1%, while the Ocean Liner was up 0.5%. Both portfolios are bac...

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Eight of the twelve major stock markets that we monitor went up last wee...