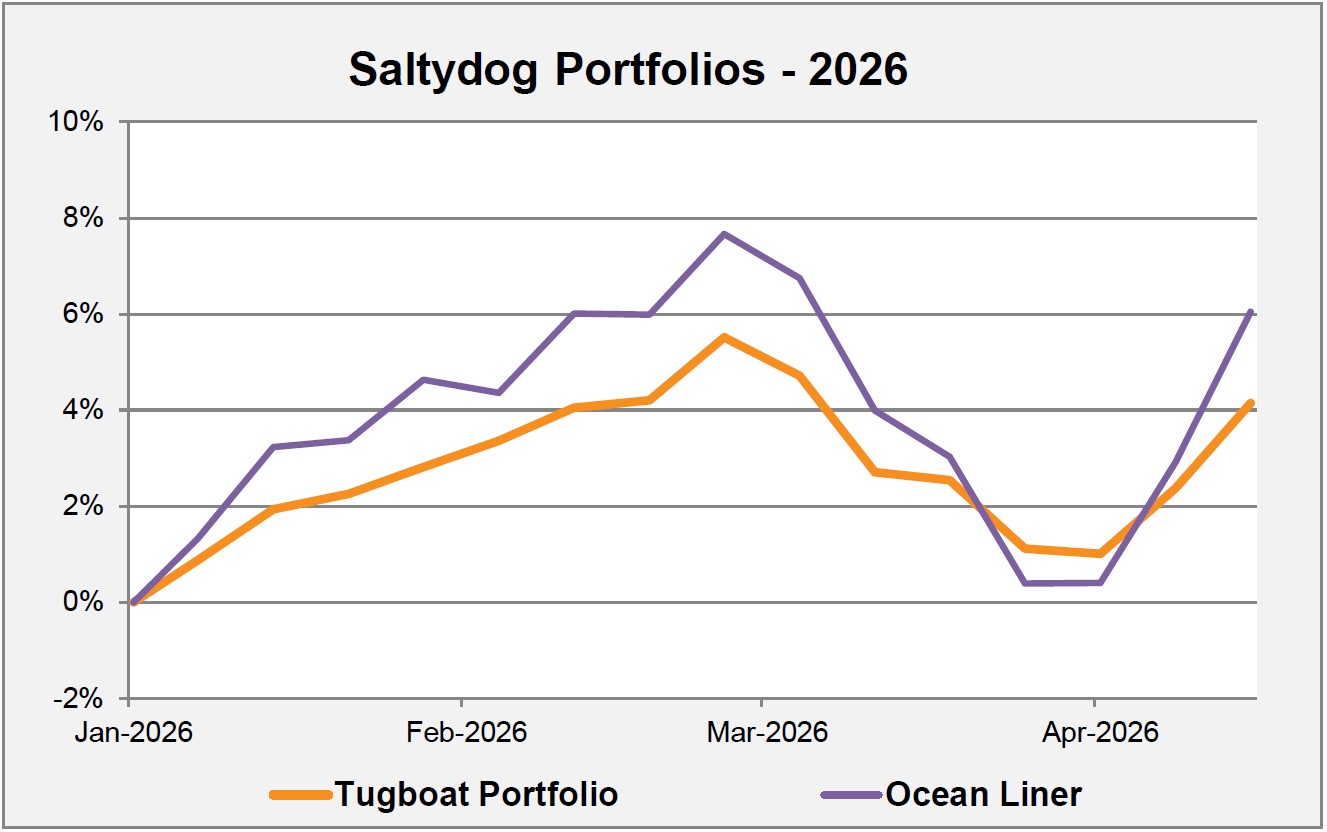

Good evening,The latest weekly portfolio updates are now available.Both portfolios have rebounded strongly during the first two weeks of April. Since this time last week, the Tugboat has risen by 1.7% and the Ocean Liner has added a further 3....

Good evening,The latest weekly portfolio updates are now available.Both portfolios have rebounded strongly during the first two weeks of April. Since this time last week, the Tugboat has risen by 1.7% and the Ocean Liner has added a further 3....

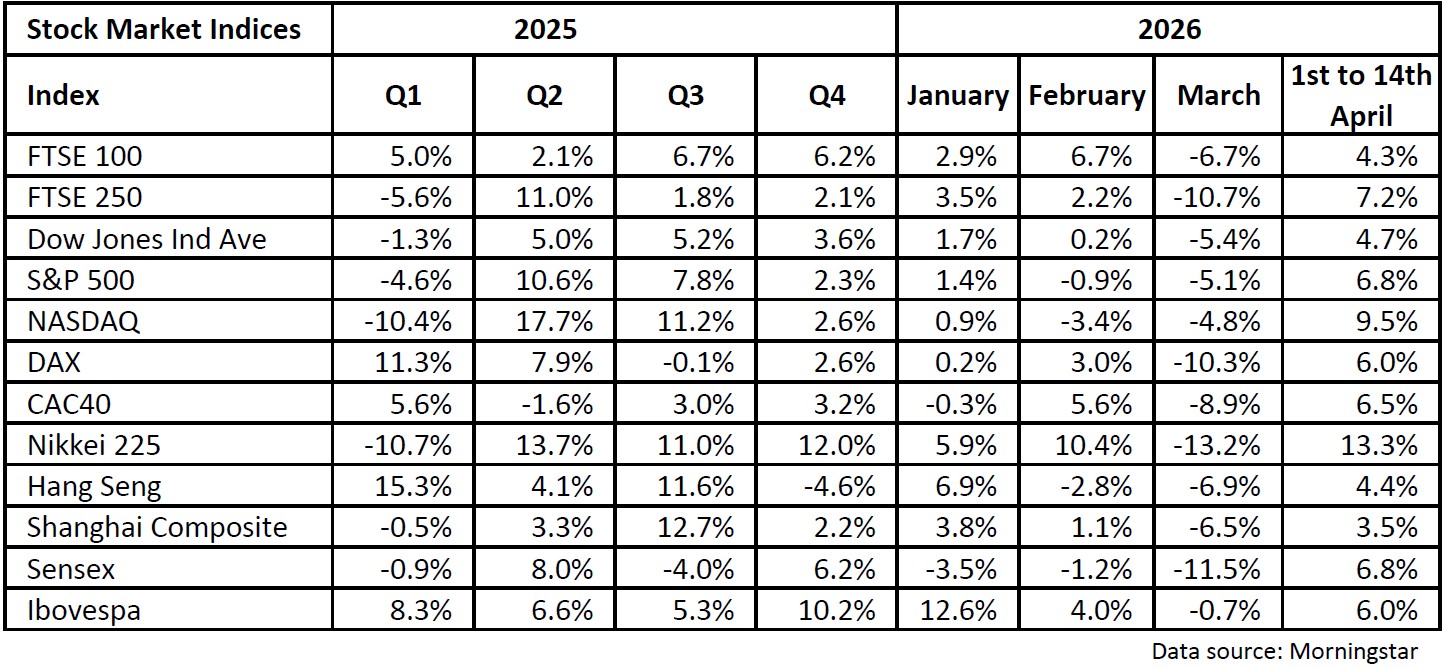

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Stock markets continued to move higher last week, building on the recove...

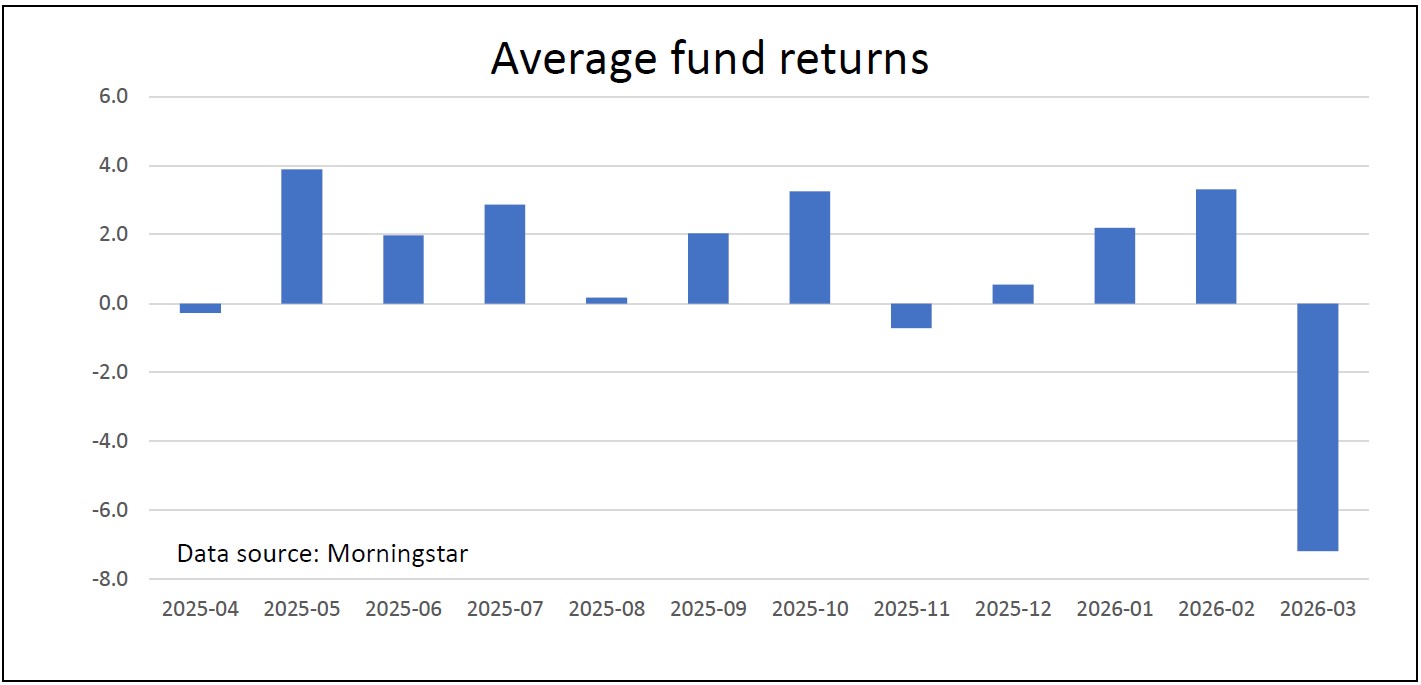

Good evening,The latest weekly portfolio updates are now available.Last month was by far the worst that we have seen for several years. There are lots of ways you can measure it, but here is a simple chart showing the average one-month return ...

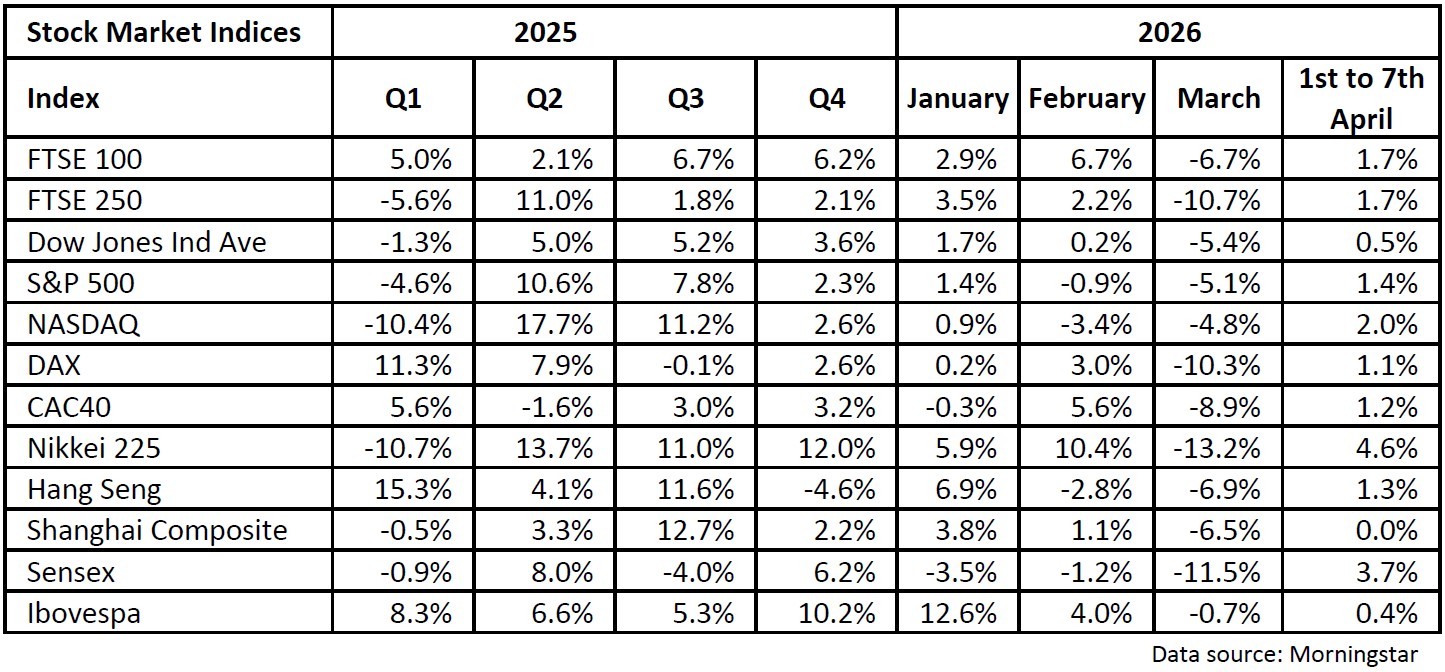

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Stock markets rallied last week, although it was a shortened trading per...

Good evening,The latest weekly portfolio updates are now available.After another difficult week for stock markets around the world, it was encouraging to see this morning that the demonstration portfolios were holding up relatively well. The T...

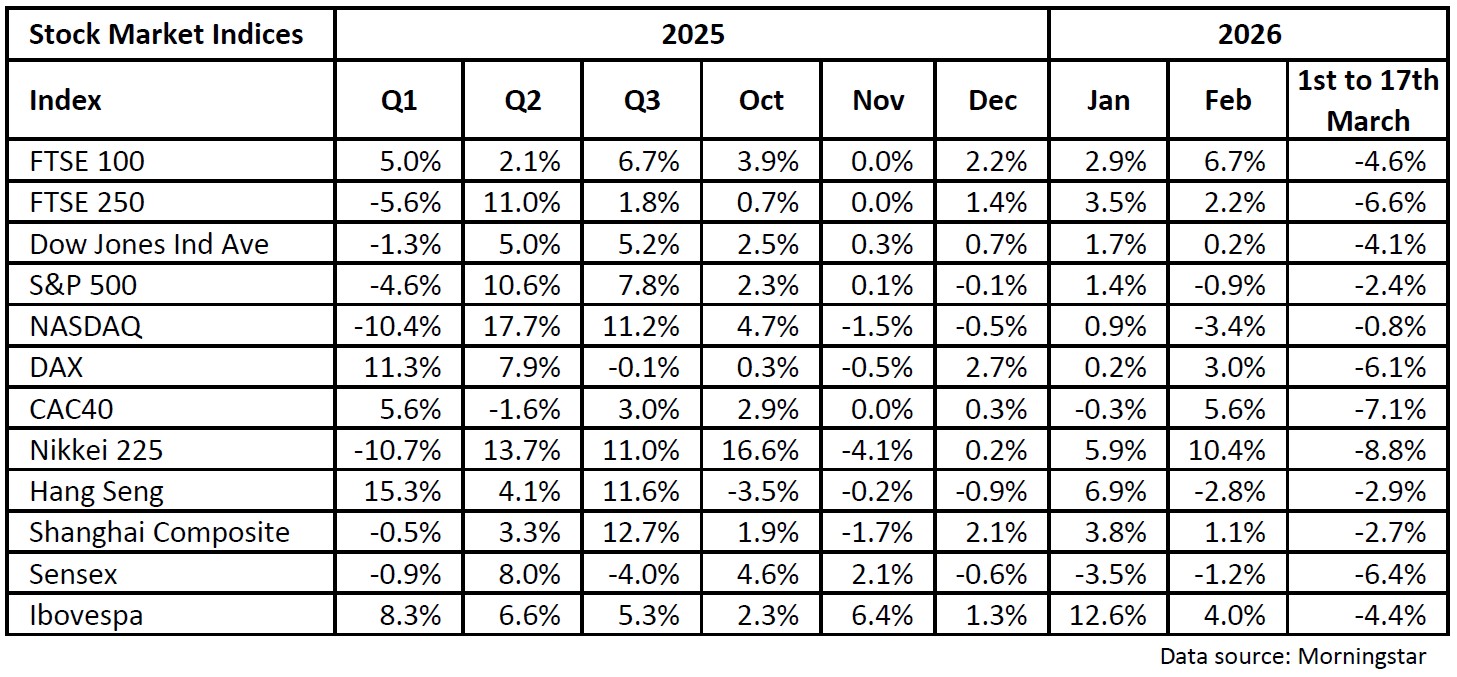

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Most of the stock markets that we track went down last week, adding to t...

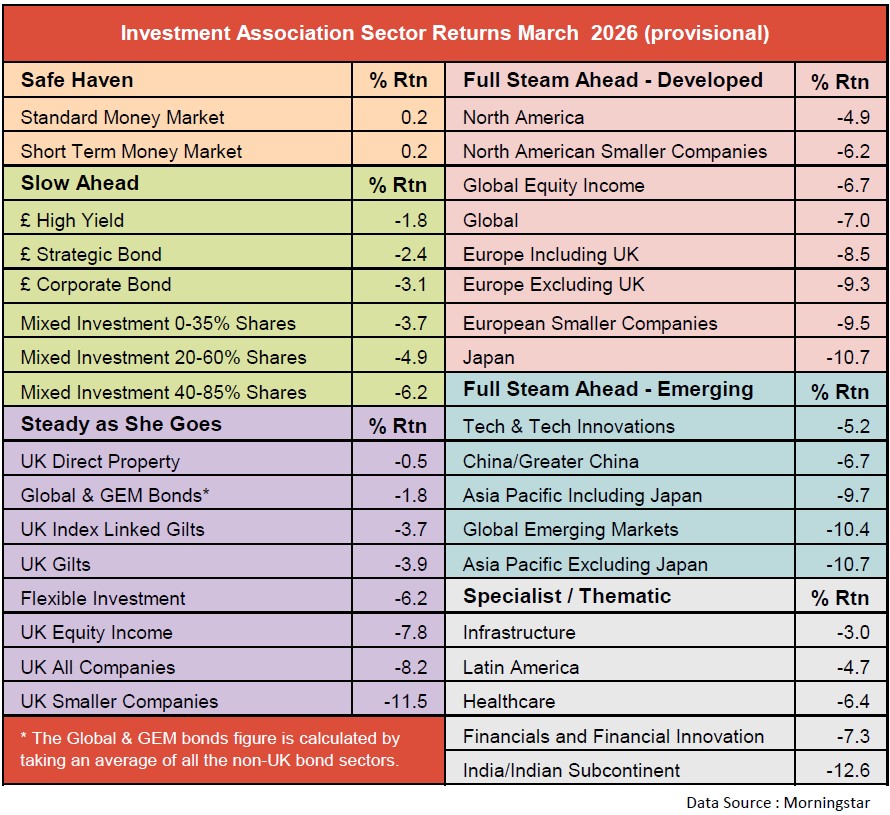

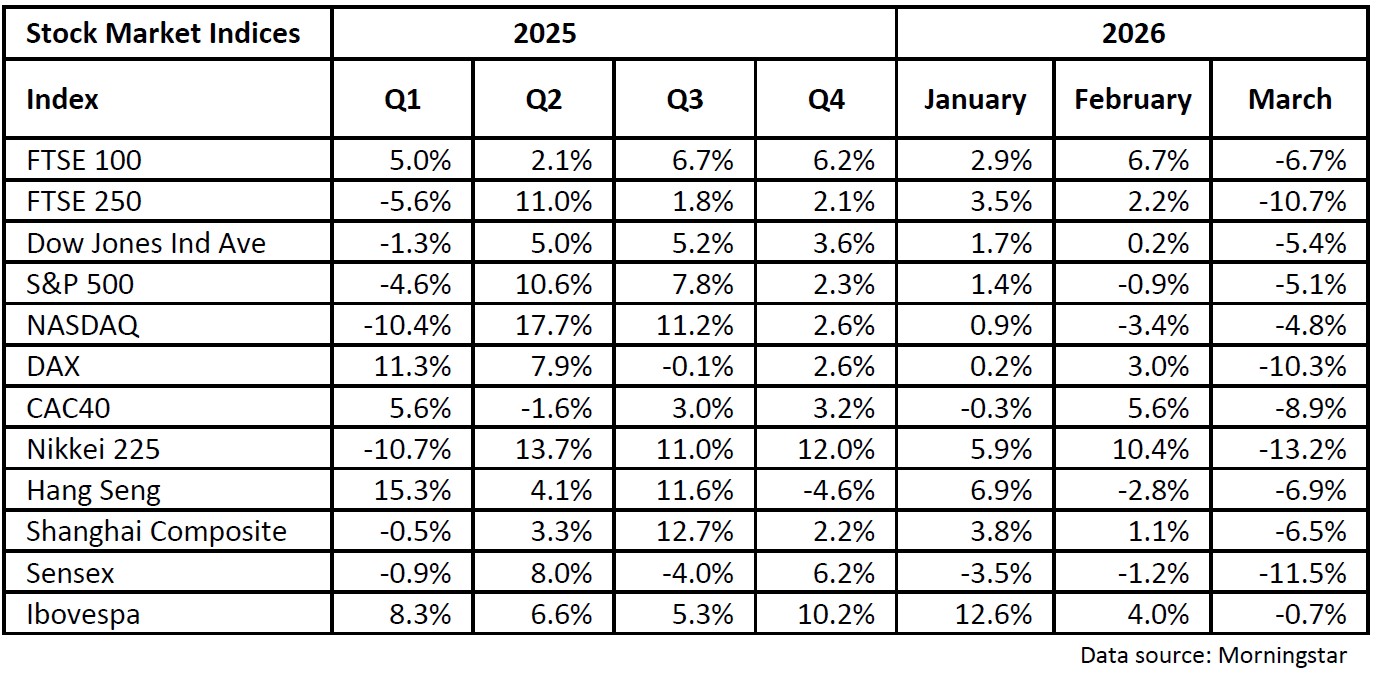

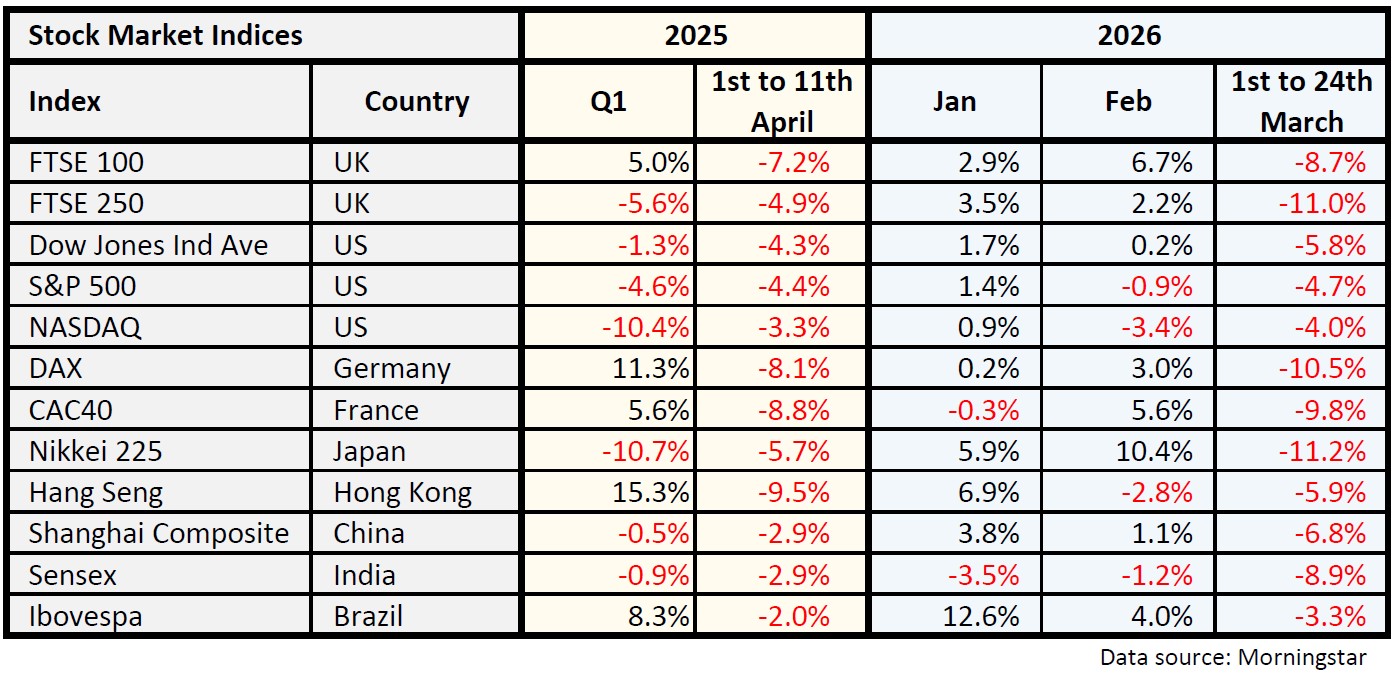

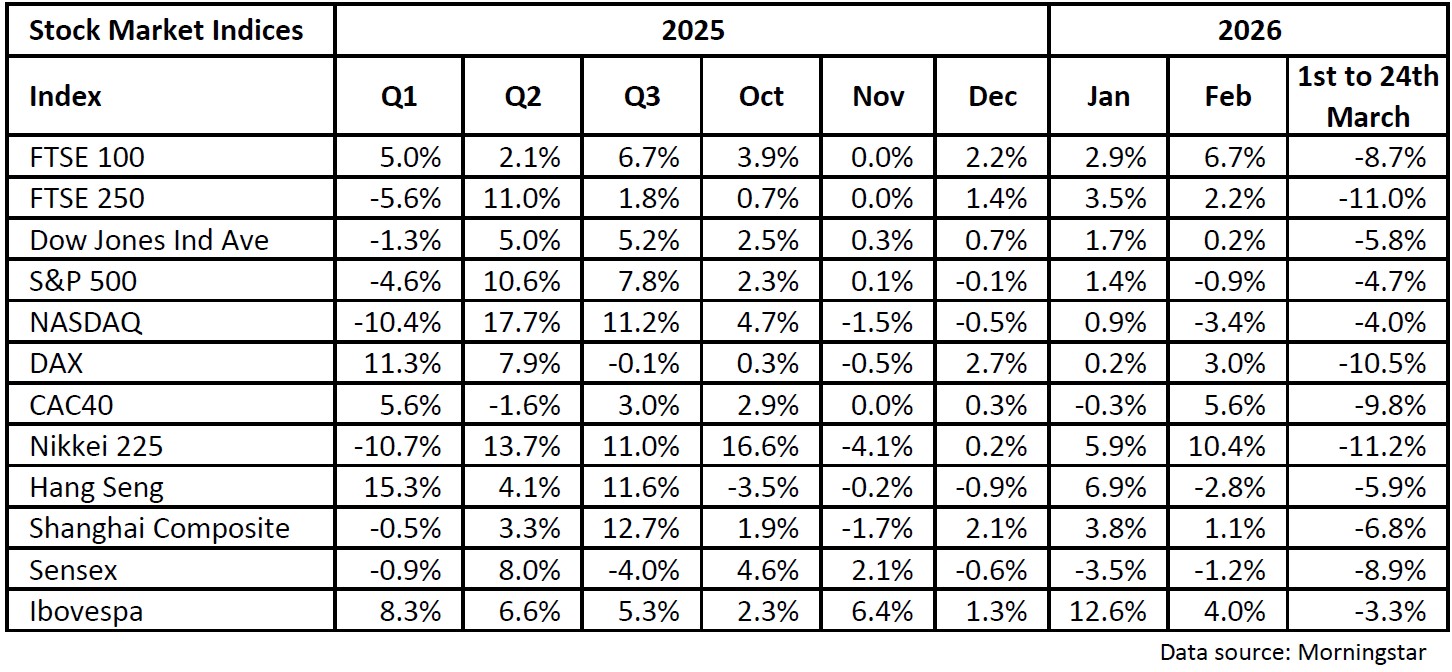

Good evening,The latest weekly portfolio updates are now available.It's been a tough week for both portfolios, with the ongoing war in the Middle East weighing heavily on the markets. As I highlighted this morning, all of the sectors went down...

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Stock markets fell sharply last week, and although there has been a mode...

Good evening,The latest weekly portfolio updates are now available.Over the last couple of weeks, nearly all of the funds that we monitor have gone down. The main exceptions have been the money market funds and the energy funds – WS Guinness G...

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Stock markets remain unsettled, although there has been a modest recover...