Good evening,The latest weekly portfolio updates are now available.Since this time last week, our Tugboat portfolio has gone up by 0.3%, and the Ocean Liner has risen by 0.5% - nearly all of our individual holdings have also gone up.This week...

Good evening,The latest weekly portfolio updates are now available.Since this time last week, our Tugboat portfolio has gone up by 0.3%, and the Ocean Liner has risen by 0.5% - nearly all of our individual holdings have also gone up.This week...

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Most of the major stock market indices that we monitor went up last week...

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Most of the major stock market indices that we monitor went up last week...

Good evening,The latest weekly portfolio updates are now available.It’s another one of those weeks when world events seem to be moving at such a pace that it is hard for our analysis to keep up.When I checked this morning, both of our demonstr...

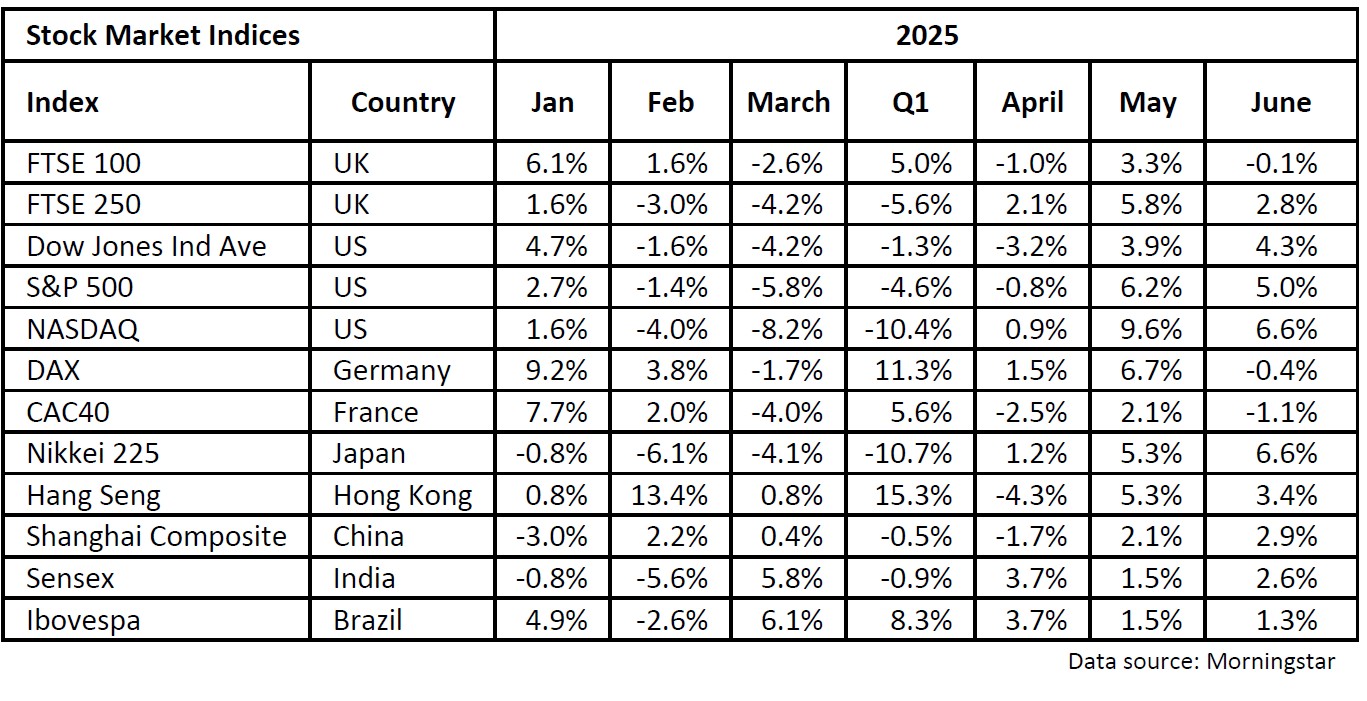

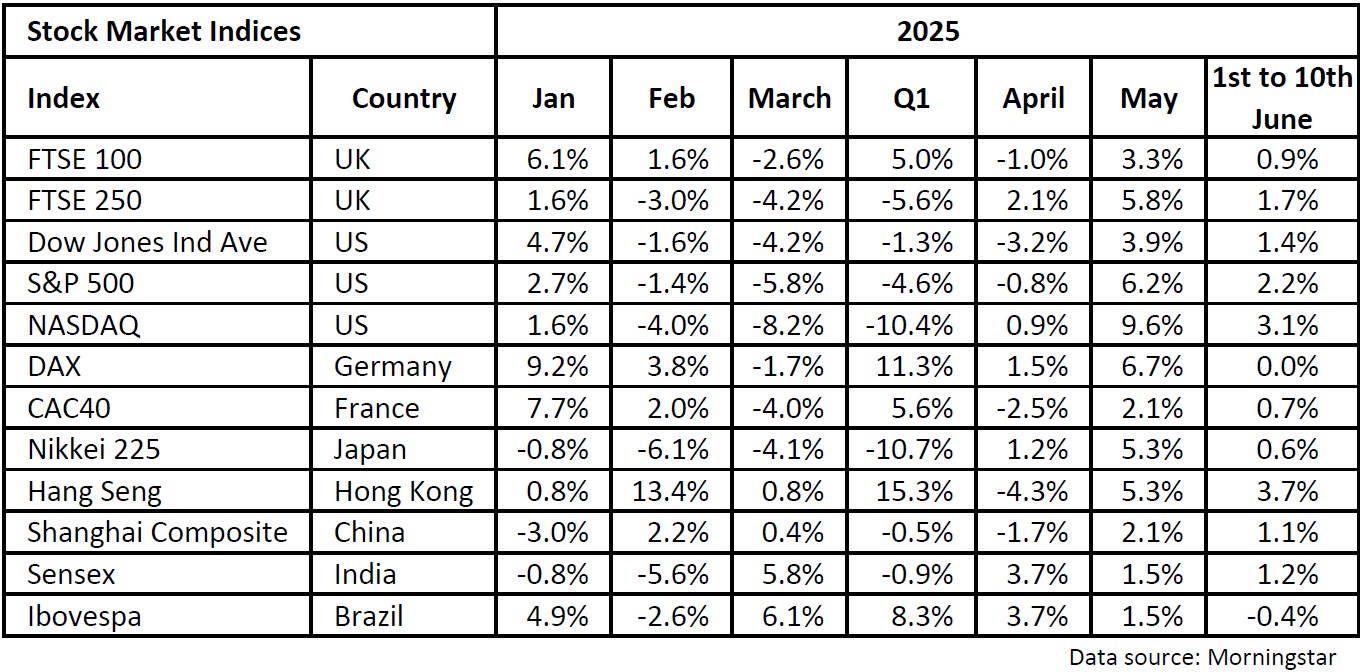

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Most of the stock markets that we track posted losses last week, but the...

Good evening,The latest weekly portfolio updates are now available.This is one of those weeks when our latest analysis, covering fund and sector performance up to the end of play last Friday, already feels out of date.Although a few of our hol...

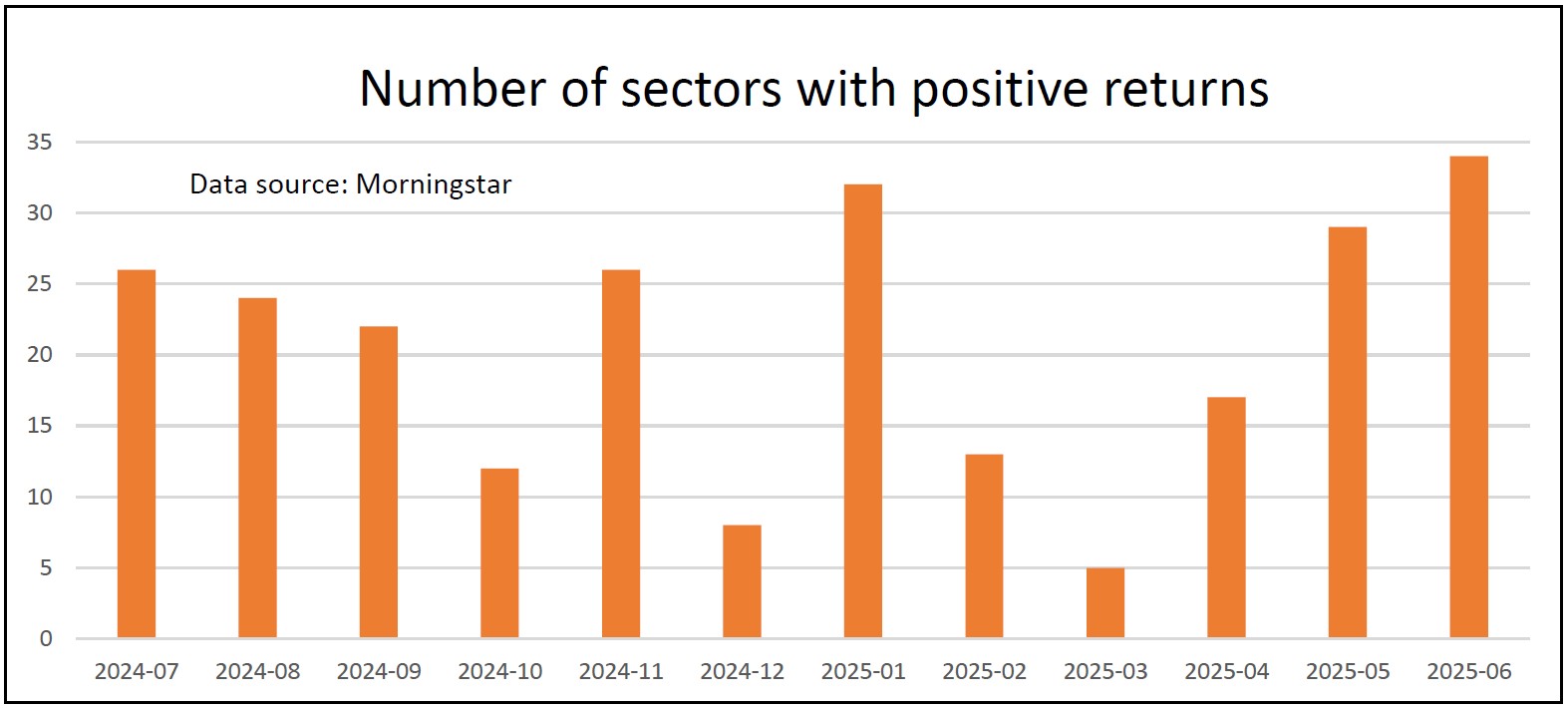

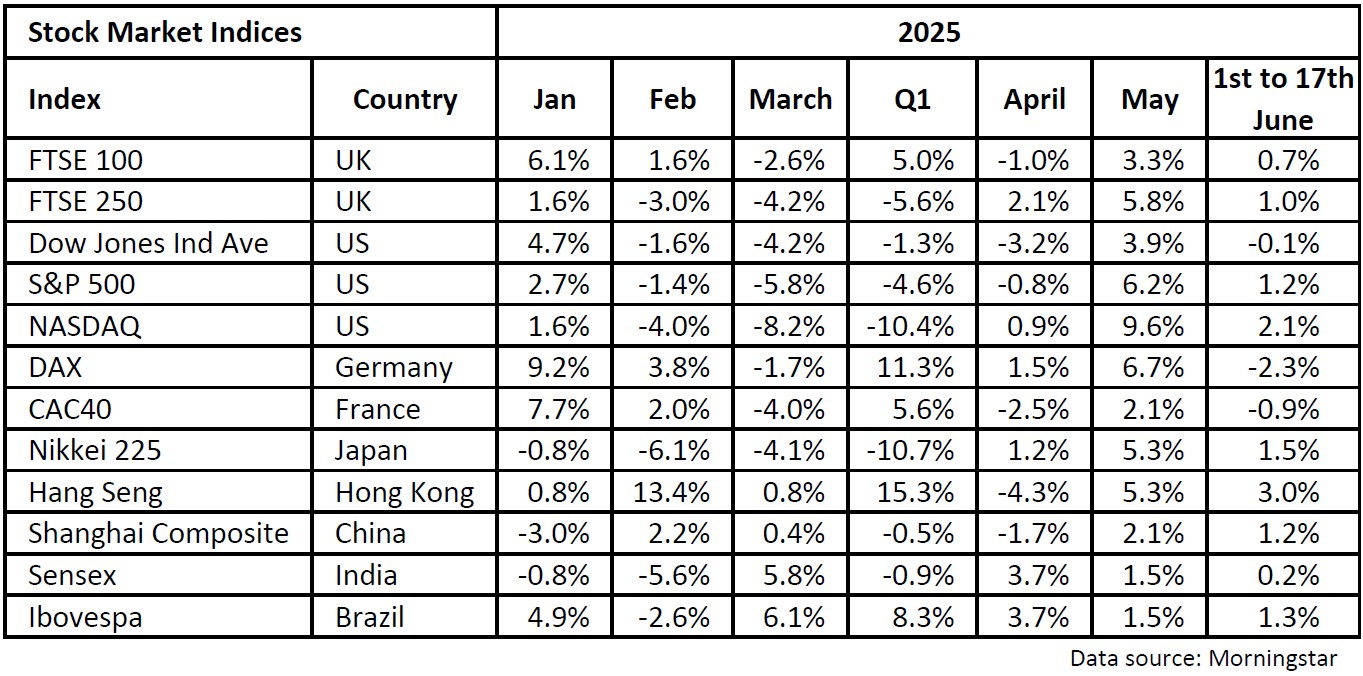

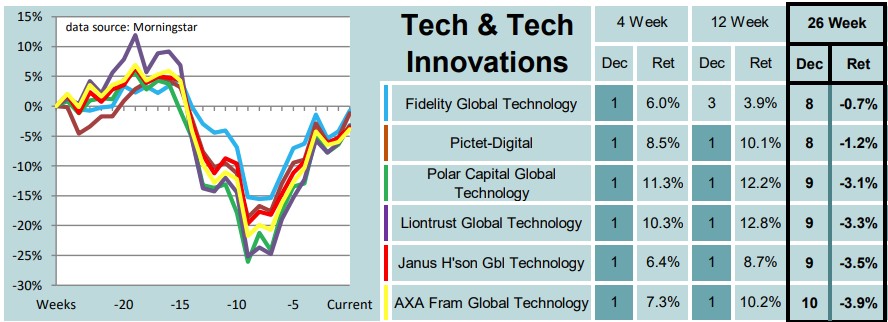

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Nearly all of the stock markets that we monitor went up in the first wee...

Good evening,The latest weekly portfolio updates are now available.It's been another good week for our demonstration portfolios - since this time last week, the Tugboat has risen by 0.4%, while the Ocean Liner has gained 0.5%.All of our holdin...

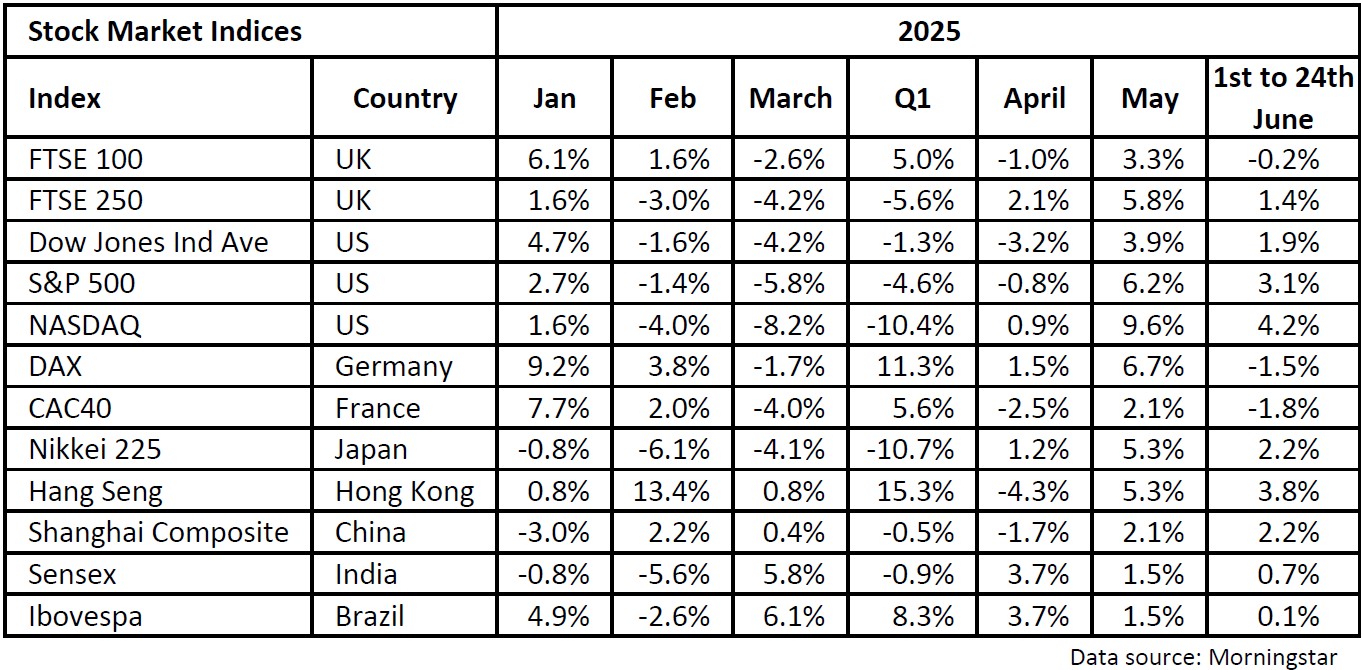

Good morning,The latest weekly data is now available.We will be doing some further analysis of the latest reports, and then decide what to do with the portfolios - more news later. Most of the global stock market indices that we track made gains last we...

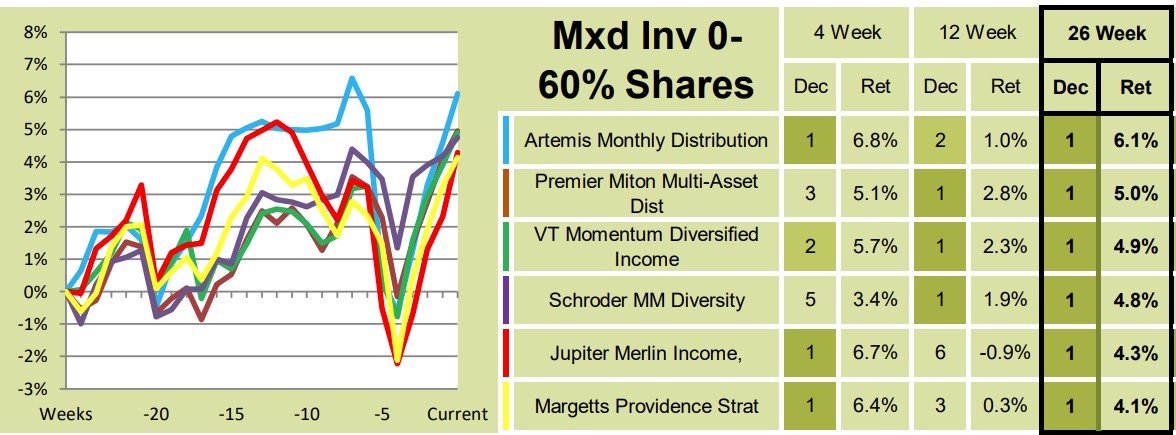

Good evening,The latest weekly portfolio updates are now available.It's been a good week for our demonstration portfolios – both are showing week-on-week gains.All of our holdings are also ahead of where they were this time last week. The sta...